Long-term notes payable are often paid back in periodic payments of equal amounts, called installments. Each installment includes repayment of part of the principal and an amount due for interest. The principal is repaid annually over the life of the loan rather than all on the maturity date. For instance, underwriters buy bonds issued by governments or corporations and accept responsibility for marketing them to investors. When market interest rates are higher than a bond’s interest rate, investors won’t pay the full par value, resulting in a discount. In some cases, the issuer of notes payable simply issues the securities at a discount.

How Discounts Impact Interest Rates

In scenario 3, there is an immediate reduction of principal because of the first payment of $1,000 made upon issuance of the note. The remaining four payments are made at the beginning of each year instead of at the end. This results in a faster reduction in the principal amount owing as compared with scenario 2.

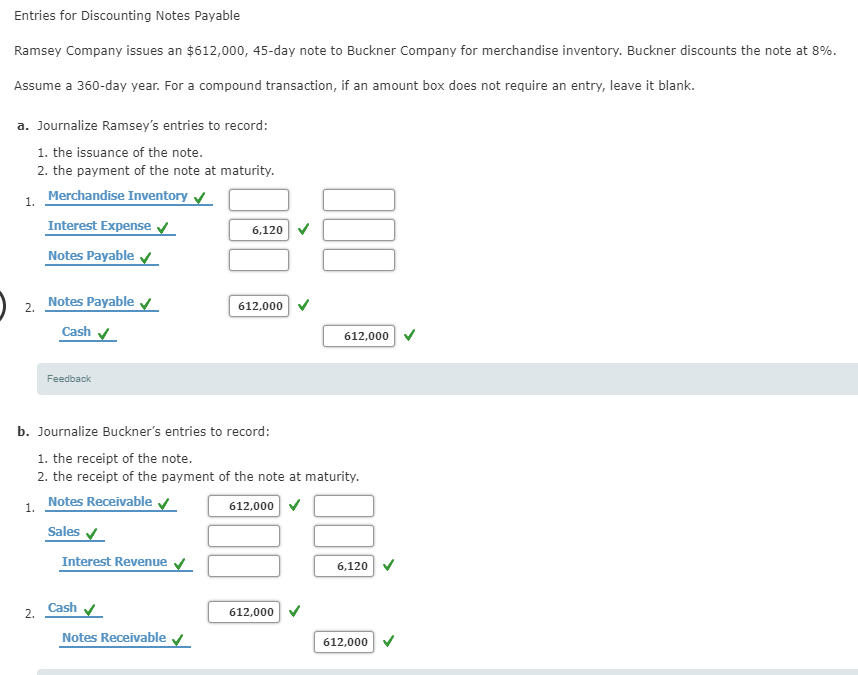

Accounting for a Discount on Notes Payable

The company can make the notes payable journal entry by debiting the cash account and crediting the notes payable account on the date of receiving money after it signs the note agreement with its creditor. Suppose a $1,000 par value bond matures in 6 months and pays 4 percent interest. The bondholder will receive $20 in interest for the six-month life of the bond. However, if the bond price is discounted to $980, the bondholder will get an extra $20 at maturity for a total of $40 in earnings. Since the price was $980, divide $40 by $980 and double the result to find the effective annual rate of interest, which here works out to 8.16 percent.

Great! The Financial Professional Will Get Back To You Soon.

Usually, any written instrument that includes interest is a form of long-term debt. The first journal is to record the principal amount of the note payable. One of the advantages of discount notes is that they are not as volatile as other debt instruments.

- This situation may occur when a seller, in order to make a detail appear more favorable, increases the list or cash price of an item but offers the buyer interest-free repayment terms.

- The note payable issued on November 1, 2018 matures on February 1, 2019.

- The amount of interest reduces the amount of cash that the borrower receives up front.

- As these partial balance sheets show, the total liability related to notes and interest is $5,150 in both cases.

- If a debtor runs into financial difficulties and is unable to pay, or fully repay, the note, the estimated impaired cash flows become an important reporting disclosure for the lender.

- This will be illustrated when non-interest-bearing long-term notes payable are discussed later in this chapter.

In the following example, a company issues a 60-day, 12% interest-bearing note for $1,000 to a bank on January 1. The premium or discount amount is to be amortized over the term of the note. Borrowers should be careful to understand the full economics of any agreement, and lenders should understand the laws that define fair practices. Lenders who overcharge interest or violate laws can find themselves legally losing the right to collect amounts loaned. This has been assumed to be calculated with a discount rate of 6%, and the difference between present value and future value has been deemed a discount. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content.

For example, on January 1, 2021, Empire Construction Ltd. signed a $200,000, four-year, non-interest-bearing note payable with Second National Bank. During 2023, Empire Construction Ltd. experienced some serious financial difficulties. Based on the information provided by Empire Construction Ltd. management, the bank estimated that it was probable that it would receive only 75% of the 2023 balance at maturity. If a debtor runs into financial difficulties and is unable to pay, or fully repay, the note, the estimated impaired cash flows become an important reporting disclosure for the lender.

They are bilateral agreements between issuing company and a financial institution or a trading partner. For example, a bank might loan a business $9,000 with a 10-year, $10,000 zero interest note. This means the company borrows $9,000 from the bank and must pay back $10,000 over the course of 10 years. The $1,000 difference between the amount received and the amount owed is considered the discount.

They are, therefore, perceived to be a safe investment for investors looking to preserve their capital in a low-risk investable security. A discount note is a short-term debt obligation issued at a discount to par. Discount notes are similar to zero-coupon bonds and Treasury bills (T-Bills) and are typically issued discount on notes payable by government-sponsored agencies or highly-rated corporate borrowers. National Company prepares its financial statements on December 31 each year. Therefore, it must record the following adjusting entry on December 31, 2018 to recognize interest expense for 2 months (i.e., for November and December, 2018).

The size of this discount is especially large when the stated interest rate on a note is well below the market rate of interest. A note payable is a loan contract that specifies the principal (amount of the loan), the interest rate stated as an annual percentage, and the terms stated in number of days, months, or years. A note payable may be either short term (less than one year) or long term (more than one year).

On the maturity date, only the Note Payable account is debited for the principal amount. A business may borrow money from a bank, vendor, or individual to finance operations on a temporary or long-term basis or to purchase assets. Note Payable is used to keep track of amounts that are owed as short-term or long- term business loans. Notes payable is an instrument to extend loans or to avail fresh credit in the company. In summary, both cases represent different ways in which notes can be written. In the first case, the firm receives a total face value of $5,000 and ultimately repays principal and interest of $5,200.

In the cash conversion cycle, companies match the payment dates with Notes receivables, ensuring that receipts are made before making the payments to the suppliers. It reflects that the company can realize the cash in a good fashion. Each year, the unamortized discount is reduced by the interest expense for the year. This treatment ensures that the interest element is accounted for separately from the cost of the asset. The agreement calls for Ng to make 3 equal annual payments of $6,245 at the end of the next 3 years, for a total payment of $18,935. The debit is to cash as the note payable was issued in respect of new borrowings.